This guide covers what SOX compliance involves in 2026, how to run an assessment, and the tools worth considering depending on where your program sits.

This guide covers what SOX compliance involves in 2026, how to run an assessment, and the tools worth considering depending on where your program sits.

TL;DR

- SOX is a U.S. federal law that holds public companies accountable for the accuracy of their financial reporting, with personal CEO and CFO certifications and tested internal control over financial reporting (ICFR).

- Three control families do most of the work: entity-level controls covering governance, business process controls sitting inside cycles like revenue and procurement, and IT general controls covering the systems' financial data flows through.

- A risk-based, top-down approach is the SEC and PCAOB-endorsed way to scope SOX, starting with the financial statement assertions that matter and working down to the controls that mitigate material misstatement risk.

- The ideal SOX compliance software depends on program maturity, from spreadsheets at small pre-IPO scopes to dedicated SOX platforms, with connected work management platforms like SmartSuite (that’s us!) suiting teams that want SOX to live alongside the rest of their compliance work.

What is SOX compliance?

SOX compliance means meeting the requirements of the Sarbanes-Oxley Act of 2002 (Public Law 107-204), the U.S. federal law passed after the corporate collapses of the early 2000s.

It applies to publicly traded companies on U.S. exchanges, their external auditors, and certain subsidiaries.

There are a few sections that do most of the practical work:

- Section 302 requires the CEO and CFO to personally certify, every quarter, that the financial statements are accurate and that they've reviewed the controls behind them.

- Section 404 requires management to assess the effectiveness of ICFR, and for accelerated filers, the external auditor has to issue its own opinion on those controls.

- Section 906 adds criminal penalties for false certifications, with prison time on the table for willful violations.

- Section 802 covers document retention and tampering.

In practice, SOX compliance is the work of designing financial controls, running them, capturing evidence, and proving they did their job when the auditors show up.

What are the different types of SOX compliance?

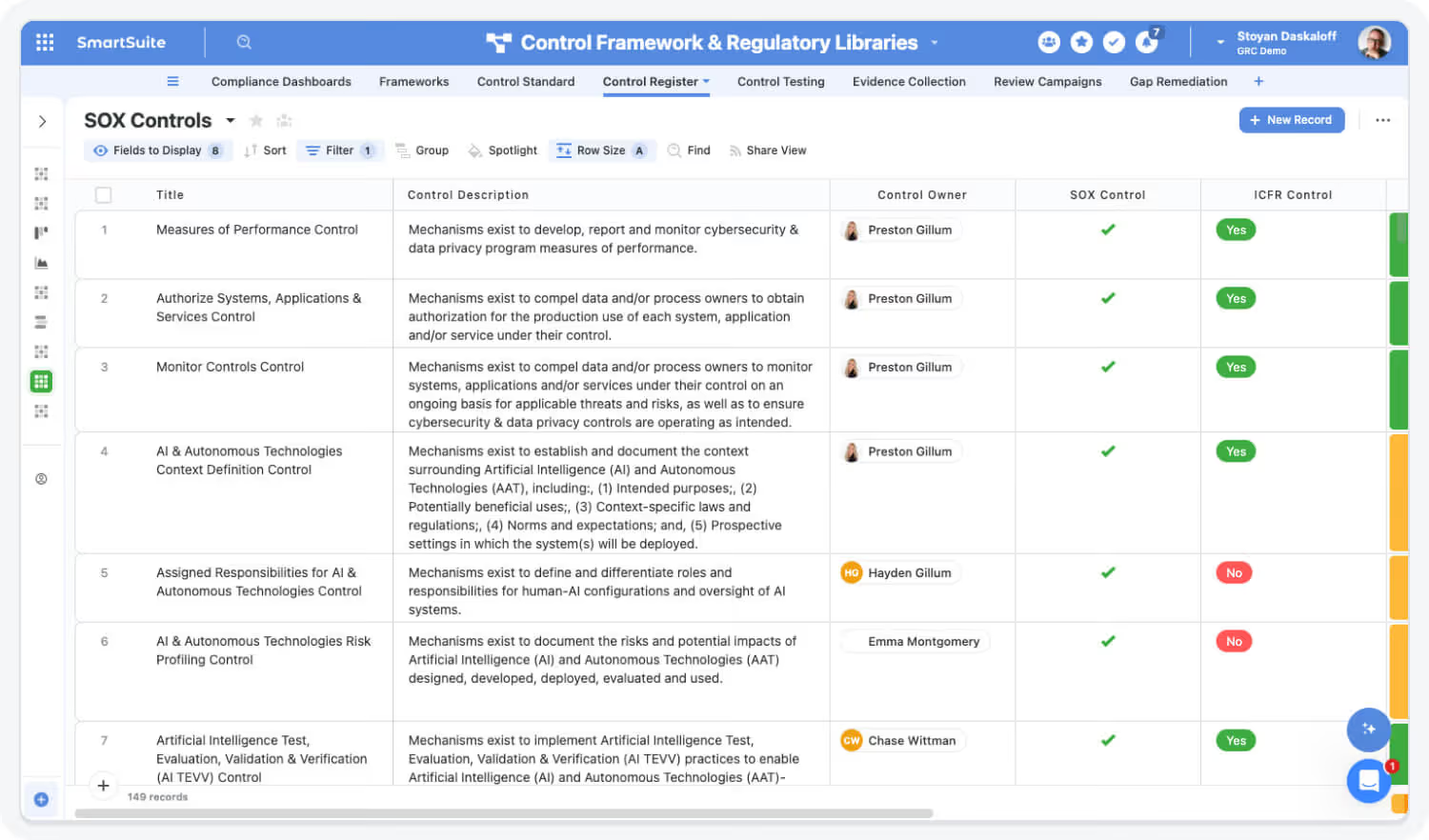

The most useful way to slice SOX is by control type, because that's how testing, evidence, and ownership get organized once a real program is running:

- IT General Controls (ITGCs) cover the systems where financial data lives or moves.

Three subdomains do the bulk of the testing: access management, change management, and IT operations like backups and scheduled jobs.

Auditors get to ITGCs early, before they touch process-level controls, because if an ITGC fails, every application control sitting on top of that system gets called into question.

- Business Process Controls (BPCs) sit inside the financial processes themselves.

Sometimes called application controls or process-level controls.

Order-to-cash, procure-to-pay, hire-to-retire, record-to-report: each cycle has its own preventive and detective controls that catch errors before they hit the general ledger.

A three-way match between purchase order, receipt, and invoice is a process control.

So is segregation of duties between the person posting a journal entry and the person approving it.

- Entity-Level Controls (ELCs) sit above both and govern the environment everything else operates in.

This is where the code of conduct, board oversight, internal audit function, whistleblower channel, fraud risk assessment, and period-end close governance all live.

When ELCs are strong, auditors can rely on less granular testing across the rest of the program. When they're weak, the rest of the testing gets deeper, more expensive, and slower.

What are the benefits of SOX compliance?

Beyond the legal floor, a working SOX program creates value in places finance teams don't always brag about:

- Cleaner financial close cycles, because the controls that prevent errors during the period also speed up the close at quarter-end.

- Better M&A readiness, both as a buyer integrating a target's controls and as a seller whose numbers hold up under diligence without months of clean-up.

- Fewer restatement fire drills, which are expensive, distracting, and brutal on stock price when they happen.

How can you approach SOX compliance?

The SEC and PCAOB both endorse a top-down, risk-based approach, and it's the most defensible way to scope a SOX program in 2026.

The logic is that you want to start with the financial statement assertions, work down through the significant accounts and disclosures, identify the processes and systems that affect them, and only test the controls that mitigate the risk of material misstatement.

Done well, this shrinks the control population to what matters.

Done badly, you end up testing every control in the building every year, and your program drowns under its own weight.

A few principles separate scaling programs from suffering ones based on what I’ve seen in the compliance industry:

- Materiality drives scope, not the other way around.

If an account sits below the materiality threshold and doesn't carry qualitative risk like related-party, fraud-prone, or complex accounting, it doesn't belong in scope.

- Control rationalization is an ongoing discipline.

Most programs accumulate controls over years and never prune them.

The result is 40 controls in a process that only needs 18. A yearly rationalization pass keeps the testing population honest.

- Ownership has to be explicit at the control level.

A vague "the finance team owns it" doesn't survive turnover.

A named control owner with a documented backup and a real testing schedule does.

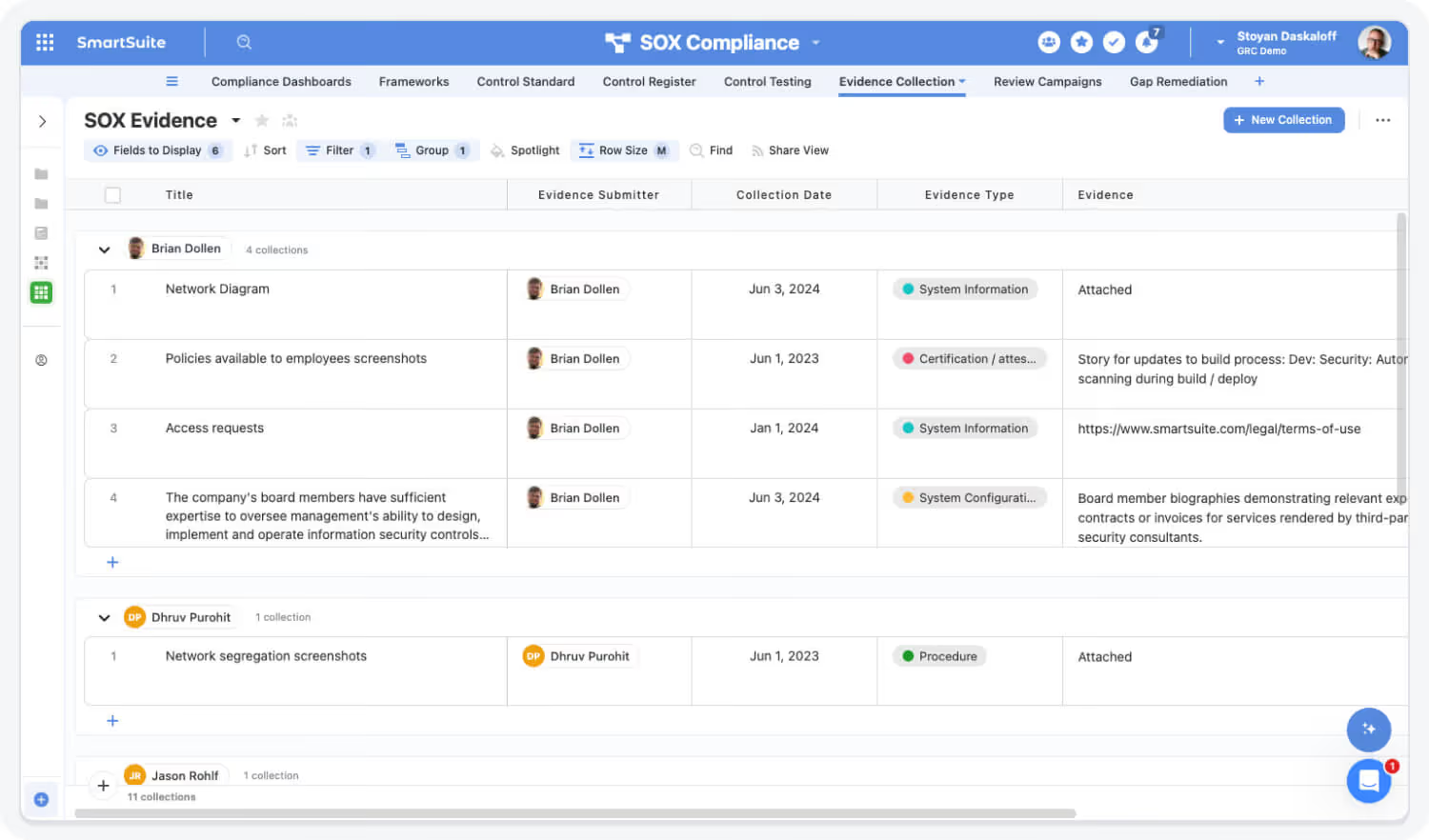

- Evidence collection should be designed, not improvised.

If you're screenshotting reports at quarter-end to gather evidence, the close gets chaotic. If evidence is captured as the control runs, the close stays quiet.

- Integration with the rest of GRC compounds the benefit.

SOX overlaps heavily with SOC 1, SOC 2, ISO 27001, and internal audit work.

Teams that map controls once and reuse them across frameworks cut their evidence burden meaningfully.

Who actually runs SOX inside a company?

SOX is a team sport. The role names vary by company, but the lines of responsibility don't.

The cleanest way to think about it is the Three Lines Model, an Institute of Internal Auditors framework that replaced the older "Three Lines of Defense" structure in 2020.

Mapped onto SOX, it looks like this:

The Board and Audit Committee (governance)

The Audit Committee oversees the SOX program from the top.

They review material weaknesses, hire and manage the external auditor, and oversee program integrity at the board level.

SOX Section 301 made audit committee independence a listing requirement, not a recommendation.

The CEO and CFO (accountability)

The CEO and CFO personally certify the financial statements and the controls behind them every quarter, with Section 906 putting criminal liability on the line for false certifications.

First line: control owners

This is where controls actually run.

- The AR manager owns revenue recognition controls.

- The IT director owns change management.

- The payroll lead owns hire-to-retire.

These aren't SOX specialists; they're business operators whose day jobs include executing controls and producing evidence on request.

Second line: SOX PMO, internal controls, and compliance

The team that builds the framework, maintains the RCM, schedules testing, tracks deficiencies, advises the first line, and prepares the management assessment.

In most public companies, it reports to the Controller or CFO; larger organizations run a dedicated Director of SOX or Internal Controls.

Third line: internal audit

Internal audit may do its own testing in parallel, review the second line's work for quality, or, in some companies, perform the bulk of management testing under a "combined assurance" model.

Either way, the function reports functionally to the Audit Committee, which is what preserves its independence.

The external auditor (independent attestation)

A PCAOB-registered public accounting firm, hired by the Audit Committee, that issues an opinion on the financial statements and, for accelerated filers, a separate opinion on ICFR effectiveness under Section 404(b).

When this structure breaks down, it's almost always because the second line ends up doing the first line's job, or the third line gets pulled into operational SOX work that compromises its independence.

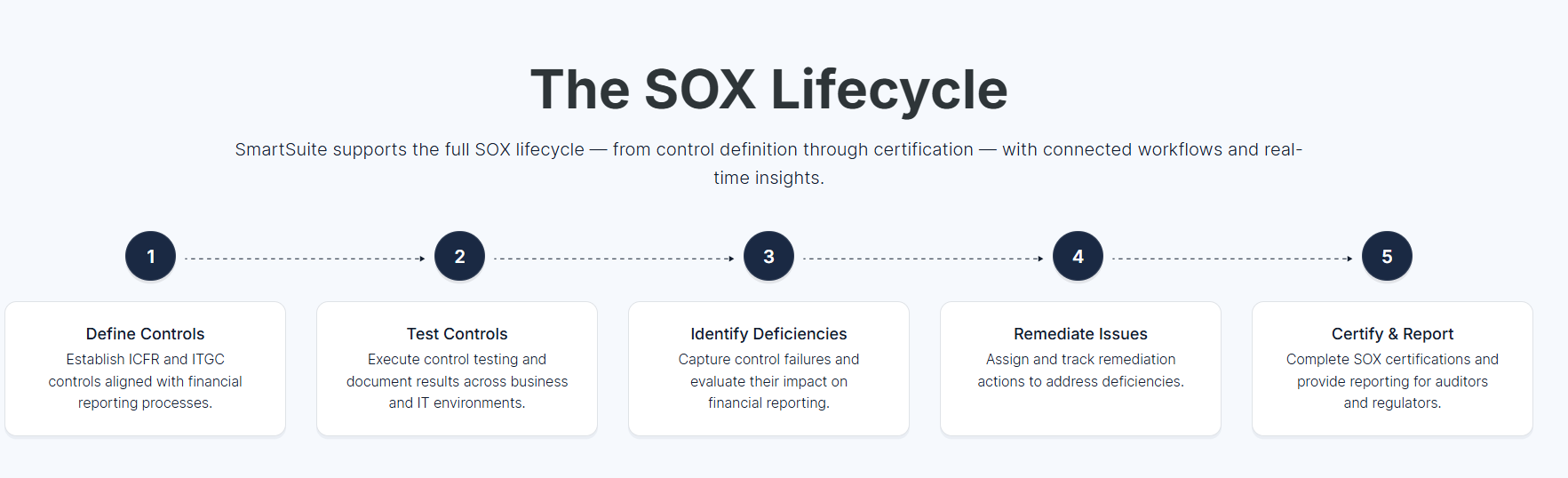

How to conduct a SOX compliance assessment

A SOX compliance assessment is the structured process of figuring out what to test, designing the tests, running them, and reporting the results:

Phase 1: Scope and design assessment

Scoping is where you decide what gets tested.

You begin at the top of the financial statements, identify the significant accounts and disclosures based on materiality and qualitative risk, map those to the processes and IT systems that feed them, and document the risks of material misstatement at each step.

For each risk, you identify the control or set of controls that mitigates it.

Design assessment then confirms that, if each control operated as documented, it would actually prevent or detect the risk.

The output is the risk and control matrix (RCM) that anchors everything downstream.

Pre-IPO companies spend most of their first six months here, because the architectural choices made now shape years of testing work afterwards.

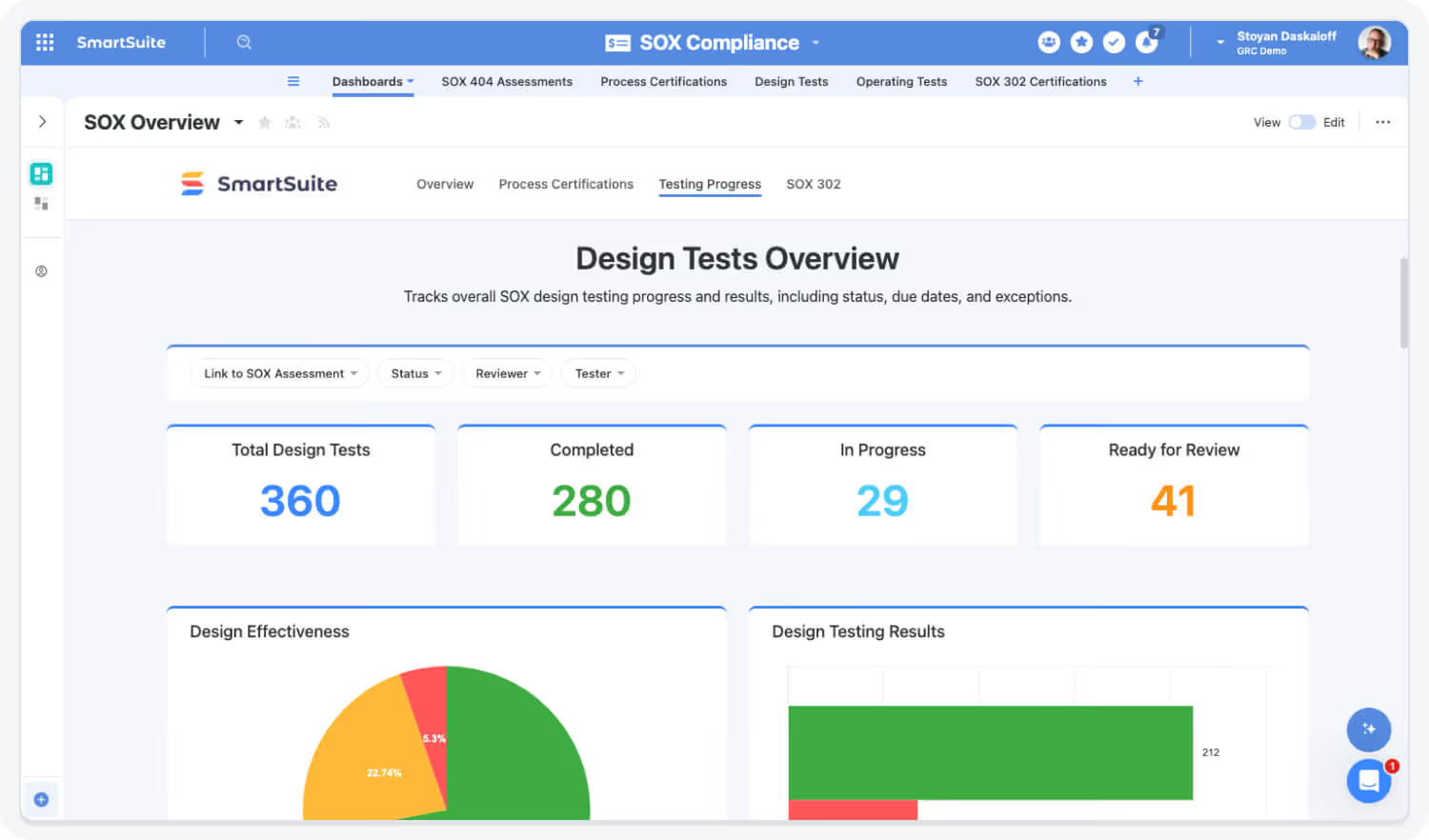

Phase 2: Test operating effectiveness

Once the design is sound, testing checks whether controls actually operate the way they're documented.

Frequency drives sample size: a daily control needs a bigger sample than a quarterly one.

The testing toolkit includes walkthroughs, reperformance, inquiry, observation, and inspection, with each control getting the test type that fits.

Most public companies test on a rolling basis, with interim testing concluding by quarter three and roll-forward testing covering the gap to year-end.

Pre-IPO teams often run "mock SOX" cycles in the year before they go live, so the first real cycle isn't also the team's first.

One of the highest-ROI moves a pre-IPO finance leader can make, in my view.

Deficiencies get logged as they're found, each one classified as a control deficiency, significant deficiency, or material weakness based on the likelihood and magnitude of the potential misstatement.

Phase 3: Remediate, report, and certify

Deficiencies don't end the assessment.

They start a remediation track that runs alongside everything else, with each one getting an owner, a corrective action plan, a target date, and a retest after the fix is in place.

- Material weaknesses get disclosed.

- Significant deficiencies get reported to the audit committee.

- Control deficiencies get tracked internally and roll up into the management assessment.

The outputs are the Section 404 management report, the Section 302 quarterly certifications, and, for accelerated filers, the auditor's separate opinion on ICFR.

Mature programs run this as a continuous loop.

New systems get scoped as they go live, remediated controls feed into next year's scoping, and continuous monitoring surfaces failures in near real-time, which beats finding out at the next testing window that a key control hasn't worked since June.

What kind of tools can you use for SOX compliance?

The tools fall into a few buckets, and which one fits depends on program scope and how connected SOX needs to be with the rest of your governance work.

Spreadsheets and shared drives

Spreadsheets are where a lot of programs start here.

Excel or Google Sheets handles the RCM, evidence drops into SharePoint or Drive folders, and a status tracker gets updated by hand.

To be fair, this can work at small pre-IPO scopes, but it will most likely break the moment you need cross-team visibility, change tracking, or auditor-ready evidence trails.

Dedicated SOX and audit platforms

Optro (formerly AuditBoard), Workiva, and Onspring were all purpose-built for SOX, internal audit, and ICFR work.

They give you structured RCMs, automated testing workflows, evidence repositories, deficiency tracking, and the auditor collaboration features mature programs need.

Enterprise GRC platforms

IBM OpenPages, MetricStream, and LogicGate take a wider view, treating SOX as one workflow inside a broader GRC suite that also covers enterprise risk, operational resilience, and regulatory compliance.

These fit large, complex organizations with the budget and IT support to back an enterprise deployment.

Connected work management platforms

A newer category where SOX workflows live alongside the rest of the business inside a flexible, no-code system.

SmartSuite works for organizations that want SOX connected to finance operations, IT change management, and broader compliance work, and it fits pre-IPO teams that want to build the program once and have it scale with the business.

➡️ Your SOX, finance, and audit teams can manage the full ICFR lifecycle in one connected workspace, from scoping and RCMs through testing, evidence, deficiencies, remediation, and management certifications.

Each SOX control connects back to the financial processes it supports and the enterprise risks it mitigates, so deficiencies carry their full upstream and downstream context, not just a control ID and a status flag.

Real-time dashboards give SOX leaders, executives, and audit committees live visibility into testing progress, open deficiencies, remediation status, and certification readiness across entities, processes, and reporting periods.

Internal and external auditors work directly in the platform through role-based access and shared evidence views, which compresses audit windows and cuts down the volume of clarification requests teams normally absorb during testing.

Built-in automation handles the recurring work like testing reminders, reviewer assignments, evidence requests, and overdue-deficiency escalations, while SmartSuite AI takes on the tedious parts like summarizing testing evidence and drafting deficiency narratives, with every approval decision staying under human ownership and a full audit log.

Pre-built SOX templates for controls, testing, evidence, and remediation shorten implementation from a multi-month rollout to something closer to a few weeks, on a SOC 2 Type II-certified infrastructure with SSO, 2FA, encryption, and role-based permissions.

It fits well for mid-market public companies, pre-IPO teams standing up their first SOX program, and finance and audit functions that want SOX connected to the rest of their compliance work.

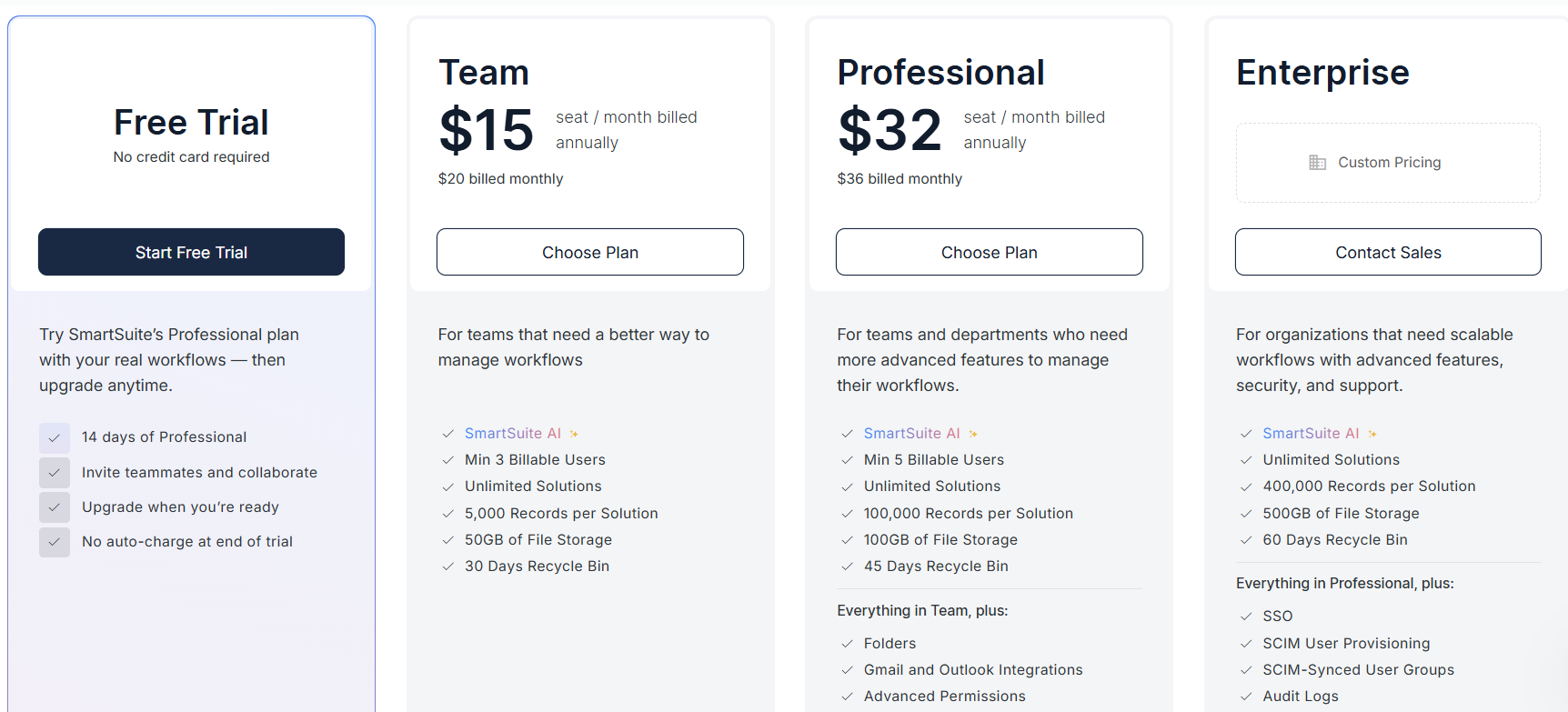

Pricing starts at $15/user/month on the Team plan, plus solution-based pricing for regulated organizations that need access structured by entity or function.

Run your SOX program on a platform built for the work

Each tool category above handles a slice of the problem.

- Dedicated SOX platforms are built for mature public-company programs with the budgets to match.

- Enterprise GRC suites suit large organizations running SOX alongside many other regulatory programs.

- Spreadsheets are fine at small pre-IPO scopes and painful everywhere else.

For mid-market public companies, pre-IPO teams, and finance and audit groups that want SOX connected to the rest of their operations, the sweet spot is a platform that handles scoping, testing, evidence, deficiencies, and certifications in one place, and doesn't need a six-month implementation to stand up.

That's the gap SmartSuite fills by giving you a no-code environment where SOX, finance, IT, and audit teams can model the program around how the business actually works, backed by enterprise-grade permissions, audit logs, SSO, and AI governance.

➡️ Start a free SmartSuite trial or book a demo to see how your team can run SOX compliance, internal audit, and broader GRC programs in one connected platform.

SmartSuite provides work platform for standardizing workflows in the following areas:

- Governance, Risk & Compliance

- IT & Service Ops

- Project / Portfolio Management

- Business Operations